⚡ Quick Answer: How to Save Money on a Low Income?

- Track your spending for 7 days to find where money silently leaks

- Build a bare-bones budget and assign every dollar a specific job

- Auto-transfer a fixed amount to savings on payday — before any bills

- Cut the 3 biggest drains: food delivery, forgotten subscriptions, bank fees

- Build a $500 emergency fund as your first savings target — nothing else until this is done

Why Saving Feels Impossible Right Now (2026 Reality Check)

You get paid Friday. By Monday, your account looks the same as before payday.

Rent. Car insurance. The electric bill. Groceries. Gas. The phone bill. Two weeks of work — gone before you blink.

Here is the hard truth: you are not failing at saving money. The financial environment is simply working harder against you than it ever has.

According to Bankrate’s 2026 Emergency Savings Report (published February 4, 2026), 59% of Americans cannot cover a $1,000 unexpected expense from their savings. A separate Empower Research study released April 15, 2026 found that 29% of Americans say they cannot afford a surprise expense of $400.

Meanwhile, the Bureau of Labor Statistics Consumer Price Index data for January 2026 confirms that consumer prices are now 26% higher than they were in 2019 — meaning your paycheck buys noticeably less than it did five years ago. Food away from home alone rose 4% in the past year.

The math feels broken — and for many people, it genuinely is.

But 27% of Americans having zero savings does not mean saving is impossible. It means most people attempt it without a system. The people building savings on a low income right now are not earning secret money. They are doing something different with the same dollars — before the bills get a chance to take everything.

This guide shows you exactly what that looks like.

What “Saving on a Low Income” Actually Looks Like

A lot of financial advice is written by people who have never had to choose between a bill and groceries. So let us be honest about the actual math.

Consider someone bringing home $1,400 per month — a realistic figure for millions of part-time, gig, and entry-level workers across the United States:

| Expense | Monthly Cost |

|---|---|

| Rent (shared apartment) | $650 |

| Groceries | $180 |

| Utilities | $90 |

| Phone | $60 |

| Transportation | $100 |

| Total Fixed Costs | $1,080 |

| Remaining | $320 |

That $320 is not spending money. It is the entire cushion for emergencies, medical needs, clothing, and every unexpected cost the month throws at you. Without a plan, most people spend it without realizing — and the month ends at zero.

Saving on a low income does not mean stashing hundreds overnight. It means deliberately protecting $50 to $100 of that $320 before it disappears. That one decision, made consistently, is what separates people with nothing saved from people slowly building a financial foundation.

How to Start: A 3-Step Beginner Strategy

Step 1 — Do a 7-Day Money Audit

Before you build a budget, you need the truth. Not what you think you spend — what your bank statement proves.

Pull up the last 30 days of transactions. Sort everything into five buckets: Housing, Food, Transport, Subscriptions, Everything Else. Add up each one.

Most people find 2–3 categories quietly draining them:

- Food delivery: Someone budgeting $200 for food often spends $320–$340 once delivery apps are counted. With food-away-from-home prices up 4% in 2026, delivery costs sting harder than ever.

- Forgotten subscriptions: The average US household carries 8–12 active subscriptions but regularly uses only 3–4. The rest silently exit the account monthly — roughly $80–$120 in total waste.

- Bank and ATM fees: $15–$25 per month for people who never notice — $300 per year for nothing in return.

You cannot fix a leak you have not found first.

Step 2 — Build a Bare-Bones Budget

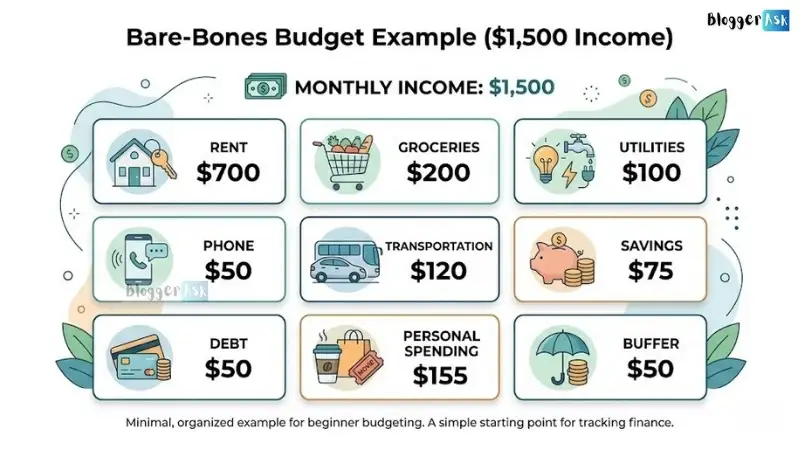

Strip everything down to essentials. Here is what it looks like for someone earning $1,500 per month:

| Category | Monthly Budget |

|---|---|

| Rent | $700 |

| Groceries | $200 |

| Utilities | $100 |

| Phone | $50 |

| Transportation | $120 |

| Essentials Total | $1,170 |

| Left to Assign | $330 |

Now assign that $330 before the month begins:

- Savings (first — always): $75

- Debt minimum payment: $50

- Personal spending: $155

- Buffer: $50

Every dollar needs an assignment. Otherwise it finds one on its own — usually something you will not remember buying three weeks later.

Step 3 — Set a Goal You Will Not Quit

The most common failure pattern: ambitious goal, burnout by week two, spend it all back. Do not try to save $400 per month on a $1,400 income on day one. That is a setup, not a strategy.

Stage it in phases:

- Months 1–2: Save $50. Just prove it is possible.

- Months 3–5: Move to $100 per month. The habit is forming.

- Month 6+: Reach $500 total — your first real financial cushion.

Start at 3–5% of take-home pay. Sustainable always beats aggressive.

3 Budgeting Methods That Actually Work

The Modified 50/30/20 Rule

The textbook version — 50% needs, 30% wants, 20% savings — breaks down on a low income. In most US cities, rent alone eats 45–55% of take-home pay. Here is the realistic version for 2026:

| Category | Realistic % | On $1,400/month |

|---|---|---|

| Needs (rent, food, bills) | 65–70% | $910–$980 |

| Wants (dining, entertainment) | 10–15% | $140–$210 |

| Savings and debt repayment | 10–15% | $140–$210 |

Even 5% saved — $70 per month — produces $840 per year. Consistency matters more than the percentage.

One rule to lock in: Every time your income goes up, send 50% of the increase directly to savings and keep the other 50% for lifestyle. If your paycheck increases by $150, move $75 to savings and enjoy the other $75. Your lifestyle improves. Your savings grows. Neither feels like sacrifice.

Zero-Based Budgeting

Every dollar gets a job. Income minus all assigned categories equals zero — not because you spent everything, but because nothing is floating around unaccounted for. For a clear explanation of this method, Investopedia’s zero-based budgeting guide is worth reading.

Unassigned money gets wasted — every time. Open EveryDollar (free version available) or a plain spreadsheet on the 1st of each month. Assign every dollar before spending one. Takes 15 minutes. Saves far more than 15 minutes of financial stress later.

The Envelope System

Withdraw cash for variable categories — groceries, gas, eating out. Put the budgeted amount into labeled envelopes on payday. When the envelope is empty, that category is done for the month. No exceptions.

This works because of psychology, not math. Handing over the last $30 from a grocery envelope feels like a real loss. Tapping a card for the same amount does not. Most people who try this report spending 15–20% less in variable categories during their first month — without any extra willpower required.

18 Practical Ways to Save Money on a Low Income

1. Cut Subscriptions First — 10 Minutes, $500+ Per Year

The average American pays for 8–12 subscriptions and actively uses 3–4. Cancel anything untouched in the last 30 days. Choose one streaming service and rotate quarterly. This single change saves $40–$70 per month.

2. Slash the Grocery Bill Without Eating Worse

- Store brands cost 20–40% less than name brands for the same product. On a $200 budget, that is $40–$80 back per month.

- Meal prepping 5 meals on Sunday ($25–$35 total) replaces $50–$80 in weekday delivery orders.

- Frozen vegetables cost $1.50–$2.00 per bag and last weeks. Fresh broccoli costs $2.50–$3.50 and is gone in 4 days. Same nutrition, 40% less cost.

- Hungry shoppers spend approximately 17% more. Write your list at home on a full stomach.

3. Rent Is More Negotiable Than You Think

Adding a roommate saves roughly $600 per month on a shared $1,200 two-bedroom apartment — that is $7,200 per year. This single change outperforms every other tip on this list combined.

If you already share, offer your landlord an 18-month lease in exchange for $25–$50 per month off. Many agree — losing a tenant costs them $1,000–$3,000 in lost rent and repairs.

4. Cut Utilities with Zero Lifestyle Change

- Unplugging standby devices (phantom power) saves $100–$200 per year

- Switching to LED bulbs (75% less electricity than incandescent) saves $8–$12 per month across 10 bulbs

- Washing clothes in cold water saves $60–$100 per year and extends clothing life

5. Cut Transportation Costs by Up to 50%

Carpooling with one coworker halves your gas bill immediately. GasBuddy helps you find the cheapest station nearby — saving $0.20 per gallon on two fill-ups per month adds up to $84–$168 per year.

6. Free Cashback Apps That Pay You Back at Checkout

- Rakuten : 1–15% cashback at 3,500+ retailers via browser extension

- Ibotta : Grocery cashback via receipt scan — regular users save $20–$40 per month

- Honey : Auto-applies coupon codes at checkout — average user saves $126 per year

- Upside : Gas and grocery cashback — $15–$40 per month

7. Never Pay Retail for Clothing

ThredUp and Poshmark sell brand-name clothing at 70–90% below retail. End-of-season sales drop prices 40–60% — buy next winter’s coat in February. Facebook Marketplace consistently has free or near-free furniture within a few miles of most people.

8. Negotiate Your Bills — Scripts That Actually Work

Internet:“I have been a customer for [X] years. I see new-customer rates advertised at $45 per month. My current bill is $75. Can you match that rate, or I will need to look at switching?” This works 60–70% of the time.

Medical bills:“Do you offer a financial hardship reduction or self-pay discount?” Most hospitals have 20–50% reduction programs. They are never advertised. You must ask directly.

Phone: Switch to Mint Mobile, Visible, or Consumer Cellular — same towers as major carriers at $15–$30 per month instead of $65–$90.

9. Eliminate Hidden Fees Draining You Monthly

- Bank maintenance fees ($12–$15/month): Switch to Chime, Ally Bank, or SoFi — all free, FDIC-insured

- Overdraft fees ($35 per incident): Maintain a $50 buffer or use a bank with no overdraft fees

- Late fees ($25–$40 on credit cards): Set autopay for the minimum on every card

- ATM fees: Get cashback at grocery checkout instead of using out-of-network ATMs

10. Stop Lifestyle Inflation Before It Stops You

When income rises, the pull to upgrade everything is immediate. This is how people earning $60,000 end up with the same savings as when they earned $35,000.

Rule: Direct 70% of any raise to savings or debt repayment. Spend the remaining 30% on lifestyle. On a $200 per month raise — $140 to savings, $60 to enjoy. Over one year: $1,680 saved while genuinely feeling the raise.

11. Use the Library — It Is Completely Free

Public library cards unlock free access to: physical and digital books, audiobooks (via Libby/OverDrive), streaming services (Kanopy for films), language learning apps (Mango Languages), digital magazines, and in some cities — museum passes. Most people pay for several of these separately.

12. Buy Generic Medication

Generic drugs contain the same active ingredients as brand-name versions at 80–85% lower cost — confirmed by the FDA’s generic drug facts page. A $40 brand-name medication often has a $6–$8 generic equivalent at the same pharmacy. Always ask your pharmacist.

13. Refinance or Consolidate High-Interest Debt

If you carry credit card debt at 20–29% interest, a personal loan at 10–15% or a balance transfer card with a 0% intro period can cut your interest costs significantly. NerdWallet’s debt consolidation comparison tool is updated regularly and free to use.

14. Automate Savings Transfers

Schedule an automatic transfer from checking to savings the same day your paycheck arrives. Even $25. Remove the decision entirely. When saving is automatic, it stops competing with spending impulses and simply happens.

15. Review Insurance Annually

Auto and renter’s insurance rates are re-evaluated by insurers regularly, but they rarely lower your rate automatically. Shopping comparison sites like The Zebra or Policygenius once a year takes 15 minutes and regularly identifies $200–$600 in annual savings.

16. Cook in Bulk and Freeze

Cooking a double or triple batch of a meal and freezing individual portions costs roughly the same as a single meal but eliminates the “I have nothing to eat, I will order delivery” decision. A freezer with 8–10 pre-made portions is your most effective defense against food delivery spending.

17. Cancel Gym Memberships You Do Not Use

The average unused gym membership costs $40–$60 per month — $480–$720 per year. YouTube has complete workout programs for every fitness level at zero cost. Nike Training Club and FitOn are also free.

18. Use Credit Card Rewards — Only If You Pay in Full Monthly

If you pay your balance in full every month, a no-annual-fee cashback credit card like the Citi Double Cash (2% on everything) or the Discover it Cash Back (5% rotating categories) earns $200–$400 per year on normal spending. Warning: This advice only applies if you have zero tendency to carry a balance. At 20–29% interest, rewards are irrelevant.

How to Build an Emergency Fund from Zero

Why $500 Is the Right First Target

Financial advisors recommend 3–6 months of expenses. That is correct — eventually. As a starting target for someone with no savings, it is paralyzing. Empower Research’s April 2026 data confirms the median emergency savings in America is currently just $500. That is where to start.

Most real emergencies on a low income cost under $500:

- Car tire blowout: $150–$300

- Urgent care visit: $100–$300

- Appliance repair: $100–$400

Without that buffer, every one of these goes on a credit card at 20–29% interest. A $300 problem quietly becomes $380 of debt before it is paid off. The emergency fund does not just feel better — it mathematically breaks the debt cycle.

How to Build It in Stages

| Milestone | Action |

|---|---|

| Month 1 | Auto-transfer $50 on payday |

| Month 3 | $150 accumulated |

| Month 6 | $300 accumulated |

| Tax refund (2026) | Direct $200 of your refund → $500 reached |

According to IRS filing season statistics for 2026 , the average US tax refund this year is approximately $3,462. Directing $200–$500 of it straight to savings cuts your emergency fund timeline significantly.

Where to Keep Your Emergency Fund

Not your regular checking account — you will spend it.

Open a separate high-yield savings account at a different bank with a 1–2 day transfer delay. That friction is intentional protection.

- Ally Bank — Currently around 4% APY, no minimum balance, no fees, FDIC insured

- Marcus by Goldman Sachs — Comparable APY, no fees, FDIC insured

Rates change frequently. NerdWallet maintains an updated comparison of high-yield savings accounts if you want to compare current rates before opening one.

Saving Habits That Stick

Pay yourself first. The moment your paycheck arrives — before any bill — move a fixed amount to savings. Set up a recurring bank transfer timed to payday. Takes 5 minutes to configure, runs automatically every cycle.

The 1% increase method. Start at 1% of income. Increase by 1% every two months.

- Month 1: 1% of $1,400 = $14

- Month 5: 3% = $42

- Month 13: 7% = $98

By month 13, you are saving nearly $100 per month without ever experiencing a painful jump.

Check your balance daily — 60 seconds. People who know their current balance are far less likely to overdraft or silently overspend by the end of the month.

One no-spend day per week. Pick any day. Spend nothing that day. This saves $15–$30 per week and resets your default relationship with spending without requiring any real sacrifice.

Wait 48 hours before any unbudgeted purchase over $20. Most impulse buys do not survive two days of thinking. No willpower required — just a delay.

Track progress visually. A sticky note on your wall, a savings widget on your phone home screen — seeing yourself move toward a number is what keeps you from resetting it.

How to Earn More Alongside Saving

Cutting expenses has a ceiling. At some income levels, there is genuinely nothing left to cut. Earning more does not have the same ceiling.

| Side Hustle | Weekly Time | Monthly Earnings (Realistic) |

|---|---|---|

| DoorDash / Uber Eats | 10–15 hours | $300–$600 |

| Instacart | 8–12 hours | $200–$450 |

| TaskRabbit | 5–8 hours | $150–$400 |

| Selling unused items (Facebook Marketplace) | 2–3 hours one-time | $100–$500 |

| Pet sitting via Rover | Flexible | $200–$500 |

One skill worth building in 2026: Learn basic graphic design on Canva (free, with YouTube tutorials widely available). By month 3, build 3 sample pieces. By month 4, open a Fiverr profile at $30–$50 per logo. Months 5–6: three orders per month equals $90–$150 in extra monthly income. Costs $0 to start.

Two Mistakes That Kill Most Saving Attempts

Saving Too Aggressively at the Start

A $400 per month savings goal on a $1,400 income sounds disciplined. What it actually produces: three weeks of restriction, a weekend where frustration leads to spending everything back, and zero net savings by month two.

Start at 3–5%. Build from there. Slow and consistent beats hard and brief every single time.

Ignoring Small Daily Spending

With 2026 prices, the cumulative cost of small purchases is higher than most people realize:

- $6 coffee, five days per week = $1,440 per year (coffee prices rose approximately 4.5% per BLS CPI data)

- $3 vending machine snack daily = $1,080 per year

- Buying lunch out three times per week instead of packing = $1,728 per year

That is over $4,200 gone in ways that felt like nothing individually. Making coffee at home three days instead of five saves $720 per year — while you still have coffee out twice a week.

Best Budgeting Tools and Apps (2026, US)

Note: All tools below are US-based. International readers should verify availability in their country before downloading.

YNAB (You Need a Budget) — $14.99/month or $99/year

The most effective budgeting tool for building new habits. Forces zero-based budgeting, includes a 34-day free trial, and is free for verified college students.

EveryDollar — Free (basic version)

Simple zero-based budget with manual entry. Everything a beginner needs without requiring a paid upgrade to start.

Monarch Money — $14.99/month or $99/year

The most capable replacement for Mint (which shut down in January 2024). Connects to your bank, auto-categorizes transactions, and includes forward-looking budget planning.

Copilot — $13/month (iOS only)

Clean interface, strong auto-categorization, and good subscription tracking. Best for iPhone users.

Cashback apps — Rakuten, Ibotta, Honey, Upside

All free. All stackable. Install them once and earn passively on purchases you were already making.

Frequently Asked Questions

How to save money when living paycheck to paycheck?

Start by finding the money you are already losing rather than trying to save new money. For most households in 2026, $25–$50 per month is hidden in food delivery orders, unused subscriptions, and bank fees. Audit your last 30 days of transactions, plug those leaks, and automate a $25 transfer to savings on payday before the money can be spent.

How much should I save from each paycheck on a low income?

Save a percentage, not a fixed dollar amount. Under $1,500 per month: target 3–5% ($45–$75). Between $1,500–$2,500 per month: target 5–8%. Build the habit first at a level you can sustain without quitting. Increase the percentage later.

What is the best budgeting method for beginners with no experience?

Start with the envelope system — physical, visual, and creates hard spending stops that no app can replicate. After 2–3 months, once you understand your own patterns, move to zero-based budgeting for finer control. Simple beats perfect when you are just beginning.

Should I pay off debt or build savings first in 2026?

Do both — in the right order. Build $500 in emergency savings first while paying minimums on all debts. Without that buffer, any surprise expense sends you back into debt and erases all progress. Once you hit $500, attack your highest-interest debt aggressively. Then rebuild the fund toward one month of expenses, then three.

Is $500 really enough for an emergency fund?

As a first target, yes — because it stops the most common financial emergencies from becoming debt. Most real emergencies on a low income cost $150–$400. The $500 target comes from Empower Research’s April 2026 data showing that is the median US emergency savings figure. It is a floor, not a finish line. Once you reach $500, the next target is one full month of expenses.

What are the best free budgeting apps for low-income households in 2026?

For beginners, EveryDollar’s free version is the simplest starting point. For automatic bank syncing and transaction categorization, Monarch Money and Copilot are the strongest options following Mint’s closure in January 2024. All cashback apps (Rakuten, Ibotta, Honey, Upside) are free and work alongside any budgeting method.

Final Thoughts + Your 30-Day Saving Challenge

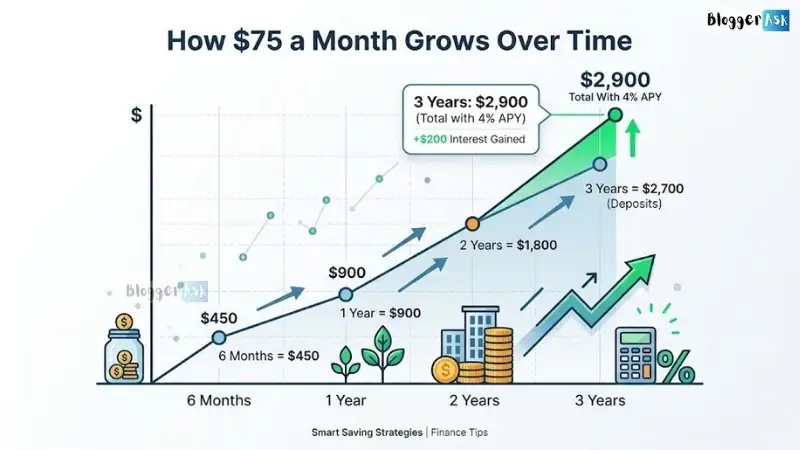

Saving $75 per month in 2026 does not sound dramatic. Here is what it actually produces:

| Timeline | Amount Saved |

|---|---|

| 6 months | $450 |

| 1 year | $900 |

| 2 years | $1,800 |

| 3 years | $2,700 |

In a high-yield savings account at 4% APY, that grows to approximately $2,900 by year three. That is the difference between a car breakdown destroying your finances and being something you handle by Tuesday.

Week-by-Week Action Plan

| Week | Exact Action |

|---|---|

| Week 1 | Pull 30 days of bank statements. Identify 3 categories where you spend more than you realized. |

| Week 2 | Cancel unused subscriptions. Choose one streaming service. Write your first bare-bones budget in EveryDollar or a notebook. |

| Week 3 | Open a free high-yield savings account at Ally or SoFi. Transfer $25 today. Set up a recurring weekly auto-transfer. |

| Week 4 | Call one bill provider and ask for a lower rate. Install Rakuten and Ibotta. Try one no-spend day this week. |

| End of Month | You have $50–$75 saved, at least one bill reduced, and a working budget in place. That is the foundation everything builds on. |

The goal this month is not to save a large amount. It is to prove to yourself that saving is possible — because once you believe that, you will not stop.

Start with $5. Start with $10. Just start today.

📖 Continue Reading

- Build Credit Score From Zero: A Complete Beginner’s Guide

- How do you raise credit score from good to excellent?

- What Is a Good Debt-to-Income Ratio for a Loan?

Disclaimer: This article is for informational purposes only and does not constitute financial advice. For guidance specific to your situation, consult a certified financial planner (CFP).

For the past decade, I’ve been researching personal finance, investing, and online income models. I break down complex money matters into simple strategies so readers can build wealth, avoid common mistakes, and make confident financial choices.