Introduction — Why Retirement Accounts Actually Matter

Let me be honest with you.

When most people first Google Roth IRA vs 401(k) for beginners, they expect a wall of confusing financial jargon. Instead, what they actually need is a simple, no-fluff explanation — the kind a financially-savvy friend would give over coffee.

That’s exactly what this guide is.

Whether you just started your first job, recently got a salary hike, or simply realized you should probably be doing something about retirement — you’re in the right place.

Here’s the truth nobody tells you early enough: the money decisions you make in your 20s and early 30s carry more weight than anything you do financially in your 40s. Because in investing, time is the most powerful variable of all.

So let’s get into it — clearly, honestly, and without the finance-bro jargon.

What is a 401(k)? — Your Employer’s Gift to Your Future Self

A 401(k) is a retirement savings account set up by your employer. It’s named after a section of the U.S. tax code — boring name, powerful tool.

Here’s how it works in practice:

Every paycheck, a portion of your salary goes directly into your 401(k) — before you ever see it hit your bank account. So if you earn $4,000/month and contribute 10%, $400 quietly goes into your retirement fund every single month.

You don’t miss it. You don’t have to think about it. It just happens.

Key features of a 401(k):

- Contributions come out of your paycheck automatically

- Your taxable income goes down (so you pay less in taxes today)

- Your money grows inside the account through investments like index funds and mutual funds

- Many employers match a portion of what you contribute — free money on top of free money

Think of it as a forced savings habit with a built-in tax bonus.

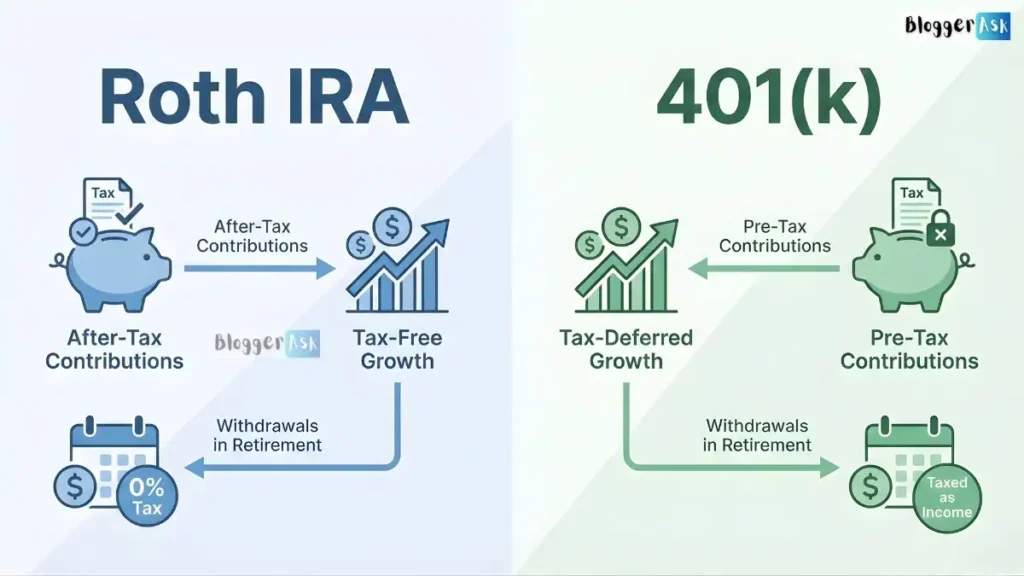

What is a Roth IRA? — The Account You Open on Your Own

Unlike a 401(k), a Roth IRA has nothing to do with your employer. You open it yourself — through platforms like Fidelity, Vanguard, or Charles Schwab — in about 15 minutes online.

You contribute after-tax money. Meaning: no immediate tax break.

But here’s the trade-off that makes it one of the most powerful accounts available, especially for beginners:

Every dollar you withdraw in retirement is 100% tax-free.

All the growth. All the compounding interest over decades. Not a single dollar taxed when you take it out at retirement.

For a 25-year-old today, that’s potentially 40 years of tax-free compounding. The math on that is genuinely life-changing.

How Taxes Work — Pay Now vs. Pay Later

This is the section where most beginners get confused. Let’s slow down.

401(k) — Pre-tax now, taxed later:

You contribute before taxes, which lowers your taxable income today. But when you retire and start withdrawing money, you pay income taxes on every dollar you take out.

Roth IRA — Taxed now, tax-free forever:

You contribute after-tax money today. No upfront deduction. But withdrawals in retirement? Completely tax-free — the growth, the earnings, all of it.

The single most important question to ask yourself:

Am I in a lower tax bracket now, or will I be in a lower bracket when I retire?

- Lower bracket now (most young beginners) → Roth IRA wins. Pay taxes at today’s lower rate and enjoy tax-free income later.

- Higher bracket now → 401(k) wins. Get the tax break today when it’s worth more.

Most people just starting out fall into the first category — which is why financial advisors consistently recommend Roth IRAs to beginners.

The Employer Match — Free Money You Should Never Leave Behind

Here’s a concept that surprises almost every beginner: employer matching.

Many companies match your 401(k) contributions up to a certain percentage. A typical structure looks like this:

“We’ll match 50% of whatever you contribute, up to 6% of your salary.”

If you earn $50,000 and contribute 6% ($3,000), your employer drops in another $1,500 — for absolutely nothing in return. That’s an instant 50% return before your investment even grows a dollar.

Not contributing enough to capture the full employer match is the #1 most expensive beginner mistake in personal finance.

Always — without exception — contribute at least enough to grab every dollar of that match before doing anything else with your money.

2026 Contribution Limits — How Much Can You Actually Put In?

Good news: the IRS raised both limits for 2026 — the most significant across-the-board increase in recent years. The 401(k) employee contribution limit increased from $23,500 in 2025 to $24,500 in 2026, and the Roth IRA limit rose from $7,000 to $7,500.

Here’s the full breakdown:

| Account | Under 50 | Age 50–59 & 64+ | Age 60–63 |

| 401(k) | $24,500 | $32,500 | $35,750 |

| Roth IRA | $7,500 | $8,600 | $8,600 |

Don’t panic if you can’t max these out. Even $100–$200/month invested consistently from your mid-20s can grow into hundreds of thousands by retirement. Start with what you can. Increase gradually.

Roth IRA Income Limits 2026 — Does Your Salary Qualify?

This is where the Roth IRA gets a little selective. Not everyone qualifies to contribute the full amount.

For 2026, the income phase-out range for single filers and heads of household making Roth IRA contributions is between $153,000 and $168,000 — up from $150,000–$165,000 in 2025. For married couples filing jointly, the phase-out range rises to between $242,000 and $252,000.

Translation:

- Single and earning under $153,000? → Full contribution allowed ✅

- Single and earning $153K–$168K? → Partial contribution allowed

- Single and earning over $168,000? → Direct contribution not allowed

High earner? Don’t worry. There’s a legal strategy called the Backdoor Roth IRA — you contribute to a Traditional IRA first, then convert it to a Roth. It’s perfectly legal and widely used.

Most beginners won’t hit these income limits early in their careers, but it’s worth knowing as your salary grows.

Key Differences at a Glance — Side-by-Side Comparison

When evaluating Roth IRA vs 401(k) for beginners, a side-by-side comparison makes the decision much clearer:

| Feature | 401(k) | Roth IRA |

| Who sets it up? | Your employer | You |

| Tax treatment | Pre-tax contributions | After-tax contributions |

| Tax benefit timing | Now (lower taxable income) | Later (tax-free withdrawals) |

| 2026 limit (under 50) | $24,500 | $7,500 |

| Employer match? | Yes (often) | No |

| Income limits? | No | Yes |

| Investment choices | Limited (employer picks) | Wide open (you choose) |

| Early withdrawal | 10% penalty before 59½ | Contributions withdrawable anytime |

| Best for | Mid-career, higher earners | Young, lower-bracket beginners |

One seriously underrated Roth IRA advantage: you can withdraw your original contributions — not earnings — at any time without penalty. This makes it a quiet emergency backup fund too.

Which One Should YOU Choose? — A Simple Decision Guide

Still unsure? Here’s a clear, no-overthinking framework:

Choose 401(k) first if:

- Your employer offers a match (non-negotiable — always grab it)

- You’re in a higher tax bracket and want to reduce your taxable income today

- Your company’s 401(k) has solid low-cost index fund options

Choose Roth IRA first if:

- You’re young, in a lower tax bracket, and want tax-free retirement income

- You want more investment flexibility and control over your money

- You’re self-employed or don’t have access to an employer 401(k)

The smartest strategy most beginners follow — do both, in this order:

- ✅ Contribute to 401(k) — just enough to get the full employer match

- ✅ Open and max out your Roth IRA — $7,500 in 2026

- ✅ Go back to your 401(k) and increase contributions with any money left

This sequence gives you the best of both worlds: free employer money and tax-free retirement income.

Can You Use Both? — The Smart Strategy Most Beginners Ignore

Yes — and this is genuinely one of the most underutilized strategies in personal finance.

You can contribute to both a 401(k) and a Roth IRA in the same year, provided you meet the income requirements for the Roth IRA.The limits don’t overlap — they’re completely separate.

In 2026, that means a combined maximum of $32,000/year in tax-advantaged savings ($24,500 in 401(k) + $7,500 in Roth IRA). Most beginners won’t hit that ceiling right away — and that’s completely fine. The point is knowing the option exists.

Even splitting a small amount between both accounts each month builds powerful habits and diversified tax advantages for the future.

Common Mistakes Beginners Make — Don’t Let These Happen to You

Understanding Roth IRA vs 401(k) for beginners also means knowing what not to do. Here are the most expensive beginner mistakes:

❌ Mistake 1: Not contributing enough to get the full employer match This is essentially refusing part of your salary. Never leave it behind.

❌ Mistake 2: Waiting until you “earn more” to start As one financial advisor noted, “If the ceiling lifts but your savings rate stays the same, you’re opting out of decades of compound interest.”Starting small at 25 beats starting big at 35 — every time.

❌ Mistake 3: Cashing out a 401(k) when switching jobs Tempting — but costly. You’ll owe income taxes plus a 10% early withdrawal penalty. Roll it over into your new employer’s plan or a personal IRA instead.

❌ Mistake 4: Leaving Roth IRA money sitting in cash Opening the account is step one. Actually investing the money inside it (into index funds or target-date funds) is step two. Cash doesn’t grow.

❌ Mistake 5: Contributing over the Roth IRA income limit If your contribution exceeds the allowable limit, the IRS imposes a 6% tax penalty on the excess amount for each year it remains in your account.Know your numbers before you contribute.

Final Thoughts

Here’s the most honest thing I can say after walking through this entire Roth IRA vs 401(k) for beginners breakdown:

The best account is the one you actually open and use.

Both are powerful. Both offer tax advantages that a regular savings account will never match. Both beat leaving your money untouched while inflation quietly erodes its value year after year.

The only real mistake is waiting.

Open an account this week. Start with $50 if that’s what you have. Set up automatic contributions so you never have to think about it again. Let compound interest silently do its work for the next 30–40 years.

Your 65-year-old self will look back at the version of you reading this right now — and feel genuinely grateful.

FAQs

What is the main difference between a Roth IRA and a 401(k) for beginners?

The biggest difference is who sets it up and how taxes work. A 401(k) is offered by your employer — contributions come out of your paycheck before taxes, so you pay taxes later when you withdraw. A Roth IRA is an account you open yourself — you contribute money after taxes, but all withdrawals in retirement are completely tax-free. Simply put: 401(k) saves you money on taxes today; Roth IRA saves you money on taxes in the future.

What are the Roth IRA and 401(k) contribution limits for 2026?

In 2026, you can contribute up to $7,500 to a Roth IRA ($8,600 if age 50+), while the 401(k) limit is $24,500 ($32,500 if age 50+). Employees aged 60–63 are eligible for an enhanced 401(k) catch-up limit of $11,250, bringing their total to $35,750. Note: the Roth IRA limit applies across all your IRAs combined — not per account.

Can a beginner have both a Roth IRA and a 401(k) at the same time?

Yes — and this is actually the smartest move for most beginners. You can have both a 401(k) and an IRA and use them together to save for retirement — the limits don’t overlap. The recommended order: first contribute to your 401(k) up to the full employer match, then max out your Roth IRA, then go back to your 401(k) if you have more to invest.

Who should choose a Roth IRA over a 401(k)?

A Roth IRA is generally better if you’re young, in a lower tax bracket, and want tax-free income at retirement. It also gives you more investment flexibility — you choose your own stocks, ETFs, and mutual funds. Roth IRAs offer a wider range of investment options than 401(k)s, plus more flexible distribution rules, including the ability to access your contributions at any time penalty-free.

What are the Roth IRA income limits for 2026?

For 2026, single filers can make full Roth IRA contributions if their modified adjusted gross income (MAGI) is below $153,000. The contribution phases out between $153,000 and $168,000. For married couples filing jointly, the full contribution is allowed below $242,000, phasing out between $242,000 and $252,000. If you earn above these limits, look into the Backdoor Roth IRA strategy.

What happens if I withdraw money from my 401(k) or Roth IRA early?

Withdrawing from a 401(k) before age 59½ typically triggers a 10% early withdrawal penalty plus income taxes on the withdrawn amount. However, a Roth IRA is more forgiving — you can withdraw your contributions (not earnings) at any time without penalty. This makes it a useful backup in financial emergencies, though it’s best to leave it untouched for retirement.

Does a 401(k) employer match count toward my contribution limit?

No — and this is great news. Employer match does not count toward your personal $24,500 contribution limit. Instead, total annual 401(k) contributions (employee + employer) must not exceed the lesser of 100% of your salary or $72,000 ($77,500 for those 50+) in 2026. So you get your full contribution limit plus free employer money on top.

Is a Roth IRA better than a 401(k) for someone just starting to invest with little money?

For most beginners starting with limited funds, a Roth IRA is an excellent first step — low minimums, full investment control, and tax-free growth over decades. However, if your employer offers a 401(k) match, always grab that first — it’s an instant return on your money. The best strategy: do both, even if contributions are small. Time in the market matters more than the amount at the start.

What is a Roth 401(k) and how is it different from a regular Roth IRA?

A Roth 401(k) is a hybrid — it combines the high contribution limits of a 401(k) with the after-tax treatment of a Roth account. The key difference from a Roth IRA: Roth 401(k)s don’t have any income limits — regardless of how much you earn, you can contribute up to the IRS limits if your employer offers one. It’s a powerful option for high earners who want tax-free retirement income.

What is the biggest mistake beginners make with Roth IRA and 401(k) accounts?

The single biggest mistake? Waiting to start. Most beginners delay because they feel they don’t earn enough or don’t understand the accounts well enough. But compound interest rewards time above everything else — even $50/month at age 22 beats $500/month starting at 35. Other common mistakes include: not contributing enough to get the full employer match, cashing out a 401(k) when switching jobs, and leaving Roth IRA funds sitting in cash instead of actually investing them.

Disclaimer: This article is for educational purposes only and does not constitute personalized financial advice. Please consult a licensed financial advisor for guidance specific to your situation.

For the past decade, I’ve been researching personal finance, investing, and online income models. I break down complex money matters into simple strategies so readers can build wealth, avoid common mistakes, and make confident financial choices.