⚡ Quick Answer: FEIE vs FTC for digital nomads

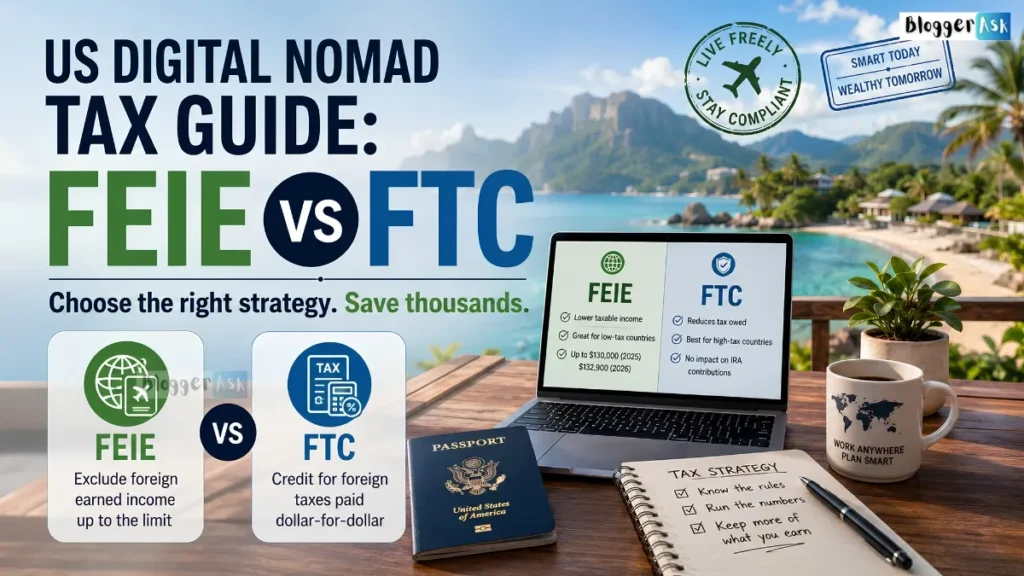

The Foreign Earned Income Exclusion (FEIE) is a rule that lets qualifying Americans abroad erase up to $132,900 (2026) of foreign earned income from their US tax return entirely. You claim it on Form 2555.

The Foreign Tax Credit (FTC) is a dollar-for-dollar credit for income tax you already paid to a foreign government. You claim it on Form 1116.

Here’s the short version of which one to reach for:

- Low- or no-tax country, income under the cap: FEIE usually wins.

- High-tax country, or income above the cap: FTC usually wins.

- Passive income, self-employment tax, or rising income: many nomads use both — FEIE on earned income up to the cap, FTC on everything else.

But for digital nomad taxes specifically, one question comes first: do you even qualify for a foreign “tax home”? If you hop between countries with no fixed base, that question often decides your bill more than the FEIE-vs-FTC choice does. This guide walks through both — in the order that actually matters.

Key Takeaways

- The Foreign Earned Income Exclusion (FEIE) removes up to $132,900 of your 2026 foreign earned income from US tax. The Foreign Tax Credit (FTC) instead credits the foreign income tax you already paid, dollar for dollar.

- Low- or no-tax country, income under the cap? FEIE usually wins. High-tax country, or income above the cap? FTC usually wins.

- Before that choice, one question matters more: can you even claim a foreign tax home? For nomads who move constantly, this — not FEIE vs FTC — often decides the outcome.

- Filing and owing are not the same. Most nomads owe $0 after FEIE or FTC. But you only reach $0 by filing and claiming it.

- FEIE doesn’t touch self-employment tax. Freelancers still owe roughly 15.3% on net earnings. Plan for it separately.

- Your federal choice doesn’t end your state residency — and it doesn’t cover the 3.8% Net Investment Income Tax on big passive income either.

Do Digital Nomads Really Have to Pay US Taxes?

Yes. The US taxes citizens and green-card holders on worldwide income, no matter where they live. It’s called citizenship-based taxation, and almost no other country does it. Moving abroad doesn’t end your filing duty. It just unlocks tools that can shrink — or erase — what you owe.

If you’re still deciding where to base yourself, compare the world’s most popular digital nomad visa programs before planning your taxes.

Why your worldwide income is reportable

It doesn’t matter if your clients are foreign, your employer is foreign, or you never touch US soil all year. If you’re a US citizen or resident alien, the IRS still wants a return covering everything you earned, everywhere.

Filing thresholds are lower than you think

A popular myth says: “I earn under the FEIE limit, so I don’t need to file.” That’s wrong.

Filing thresholds track your gross worldwide income and filing status — not the FEIE cap. For 2026, you generally must file once your gross income passes roughly your standard deduction: about $16,100 (single), $32,200 (married filing jointly), or $24,150 (head of household). Self-employed? The threshold is brutal: just $400 in net earnings.

Important: Under-reporting because you “assumed you were exempt” is one of the most common — and most avoidable — nomad mistakes.

Filing and owing are two different things

Most nomads who file correctly owe $0 in US federal income tax once FEIE or FTC kicks in. But “owing nothing” and “not filing” are not the same. You only reach $0 by filing a return and claiming the exclusion or credit on it.

Step One: Do You Even Qualify for a Foreign Tax Home?

Before you can use FEIE at all, you need a foreign tax home. Most generic “expat tax” guides skip this. It’s also the part that trips up real nomads more than anything else.

What a “tax home” actually means

Your tax home is the general area of your main place of business — not where you sleep, not where your family lives, not where your employer sits.

The IRS also wants your foreign work to be indefinite, not a short, temporary stint. A two-month contract abroad reads very differently than an open-ended arrangement. A single-location expat with one long-term job usually clears this test without thinking. A nomad changing countries every few weeks has to think hard about it.

The abode test — the part almost everyone misses

Tax home and abode are two separate tests. You must pass both. Confusing the two is one of the biggest errors in nomad tax content.

Your abode is where your economic, family, and personal ties are strongest — regardless of where you work. You cannot claim a foreign tax home for any period your abode stays in the United States, even if your work is genuinely done abroad.

This has real legal teeth, and outcomes turn on the facts. Two Tax Court cases show the line:

| Leuenberger v. Commissioner (2018) | Linde v. Commissioner (2017) | |

|---|---|---|

| Work location | Abroad | Iraq (helicopter pilot) |

| US home? | Yes | Yes (owned a home in Alabama) |

| Other US ties | US rental properties he managed, US-registered vehicles, US financial accounts, family in the US | Weaker; built real economic and social ties in Iraq |

| Foreign work | Job location only | Open-ended, renewable contracts |

| Result | Abode stayed in the US → no FEIE | Abode was abroad → FEIE allowed |

Notice the pattern. Both taxpayers owned a US home. That wasn’t the deciding factor. What mattered was which country’s ties were stronger, and whether the foreign work was indefinite or just temporary.

Does a US employer disqualify you? (No.)

Some guides claim that if your employer is US-based and you’re a W-2 remote employee, your tax home is automatically the US and FEIE is off the table. That’s an oversimplification — and, taken literally, wrong.

IRS guidance and the case law above focus on where the work is performed and where your abode sits — not whose payroll you’re on. A US employee working full-time and indefinitely from abroad can still build a foreign tax home, as long as the work is genuinely abroad and their abode isn’t in the US. Employer location is one fact worth documenting. It isn’t the deciding one.

The “itinerant worker” trap for true nomads

If you have neither a regular place of business nor a settled home, the IRS calls you an itinerant. Then your tax home becomes wherever you happen to be working at the moment.

That’s not an automatic disqualification for FEIE. But it puts more weight on documentation, because you can’t point to one obvious base. Nomads who never stay anywhere long enough to build a real footing carry genuine audit risk here — even if they clear 330 days abroad with room to spare. Remember: the abode test is a separate hurdle from day-counting.

How to document your tax home (before the IRS asks)

Build a paper trail as you go, not after the fact:

- A lease, sublease, or long-stay record showing where you’re based — even if you move around

- Business registration, client contracts, or an employment arrangement tied to a work location abroad, ideally described as indefinite

- A foreign bank account and evidence you run your financial life abroad

- A day-by-day travel log (flights, passport stamps, calendar) — this feeds both the tax-home analysis and the residency tests below

- Proof you weakened US ties: no US lease in your name, no US-registered vehicle, no immediate family left in a US home

Expert tip: Start the log on day one. Reconstructing 330 days from memory two years later is exactly what makes an audit painful.

The Two Ways to Qualify: Physical Presence vs. Bona Fide Residence

Once your tax home is settled, you must pass one of two residency tests. You only need one, not both.

Physical Presence Test

Be physically present in a foreign country (or countries) for at least 330 full days during any 12-month period. A “full day” is 24 straight hours in a foreign country. Travel days, US stopovers, and time in international waters or airspace don’t count.

Miss the threshold by even a day, and you lose the exclusion for that qualifying period. This is the test most nomads rely on, because it doesn’t require settling anywhere.

The window is flexible — use it. Your 12-month period doesn’t have to be January–December. You can choose any 12 consecutive months to hit 330 days, and you can prorate the exclusion for the days that fall in the tax year.

Example: You leave the US on May 1, 2026. By counting a 12-month window that starts in May, you can qualify sooner than if you waited for a full calendar year — then prorate your 2026 exclusion for the qualifying days.

Bona Fide Residence Test

Establish genuine residence in a foreign country for an uninterrupted period that includes one full calendar tax year (January 1 to December 31). This test weighs intent and your whole situation — a lease, local registration, community ties — instead of counting days.

It’s hard for true nomads who move every few months and never settle. That’s why most nomads default to the Physical Presence Test.

Which test fits a typical nomad?

| Physical Presence Test | Bona Fide Residence Test | |

|---|---|---|

| Based on | Day counting (330 of any 365) | Intent and settled residence |

| Works well for | Nomads moving between countries | People settling in one country long-term |

| US visits | Reduce your 330-day count directly | No fixed day limit, but must stay “temporary” |

| Best fit for pure nomads | Usually yes | Usually difficult |

FEIE vs FTC: How Each One Actually Works

Foreign Earned Income Exclusion (FEIE)

FEIE lets you exclude qualifying foreign earned income from US federal income tax entirely, up to an annual cap.

- 2025 tax year (filed 2026): $130,000 per qualifying person

- 2026 tax year (filed 2027): $132,900 per qualifying person

Married couples who both qualify can each claim their own exclusion — so a qualifying couple can shelter up to $265,800 in 2026. You claim it on Form 2555.

Qualify for only part of the year? The cap is prorated by your qualifying days.

Proration example: You qualify for 200 of 365 days in 2026. Your cap becomes $132,900 × (200 ÷ 365) ≈ $72,822.

One catch: the stacking rule. Any income left over after the exclusion is still taxed at the rate that would have applied to your full income. FEIE removes income — it doesn’t lower your marginal rate on what’s left.

FEIE only covers earned income — wages, salaries, and self-employment income for services performed abroad. It does not cover dividends, interest, capital gains, rental income, or pensions.

Foreign Housing Exclusion or Deduction

If you qualify for FEIE, you may also exclude qualifying housing costs above a base amount.

- Base amount (2026): 16% of the FEIE cap ≈ $21,264 (this base is not excludable — only costs above it count)

- General ceiling (2026): 30% of the cap ≈ $39,870, and higher in officially designated high-cost cities

Here’s the distinction most guides blur:

- Employees take a housing exclusion.

- Self-employed nomads take a housing deduction (Form 2555, Part IX).

Worked example: You’re an employee in an expensive city. Your employer-provided housing runs $45,000 for the year. Subtract the $21,264 base → $23,736 of qualifying housing, capped at your city’s ceiling. That amount is excluded on top of your FEIE.

Foreign Tax Credit (FTC)

FTC gives you a dollar-for-dollar credit against your US tax bill for income tax you already paid to a foreign government. You claim it on Form 1116.

Unlike FEIE, there’s no physical presence or residence test. You qualify simply by paying a qualifying foreign income tax on income the US also taxes. FTC covers both earned and passive income, which makes it more flexible than FEIE. Unused credits generally carry back one year or forward up to ten years.

One rule about tax treaties

You may wonder whether a US tax treaty lets you skip US tax entirely. Usually not. Nearly every US treaty contains a “saving clause” that lets the US keep taxing its own citizens as if the treaty didn’t exist. So the treaty tie-breaker residency rules that help non-citizens generally don’t rescue US citizens. FEIE and FTC — not the treaty — remain your main tools.

Side-by-side comparison

| FEIE (Form 2555) | FTC (Form 1116) | |

|---|---|---|

| What it does | Removes income from your return | Credits tax against what you owe |

| 2026 cap | $132,900 per person | No cap |

| Requires a residency test | Yes (PPT or BFR) | No |

| Requires a foreign tax home | Yes | No |

| Covers passive income | No | Yes |

| Covers self-employment tax | No | No |

| Offsets the 3.8% NIIT | No | Generally no |

| Unused amounts carry forward | No | Yes, up to 10 years |

| Best fit | Low/no-tax countries, income under cap | High-tax countries, income above cap, passive income |

| Use both in the same year? | Yes — but never on the same dollar |

The one rule that matters most: you cannot use FEIE and FTC on the same dollar of income. Exclude wages with FEIE, then credit foreign tax on income above the cap or on passive income. Never double-dip on a single dollar.

Which One Actually Saves You More Money?

The decision tree

Work top to bottom. Skipping steps is how people default to the wrong tool.

Country cheat sheet: which way each destination leans

Your host country’s real tax burden is the biggest driver. This table is a starting point, not a ruling — your actual liability depends on residency status, visa, special regimes, and local remittance rules.

| Country | Approx. top personal income-tax rate | Typical lean |

|---|---|---|

| UAE (Dubai, Abu Dhabi) | 0% | FEIE |

| Costa Rica / Panama | Territorial (foreign income often untaxed) | FEIE |

| Thailand | Up to ~35% (remittance rules matter) | Depends — often FEIE |

| Mexico | Up to ~35% | Depends |

| Portugal | Up to ~48% (special regimes may reduce) | Often FTC |

| Spain | Up to ~47% (Beckham regime ~24% flat option) | Often FTC |

| Germany | Up to ~45% + solidarity surcharge | FTC |

Example 1 — Low-tax country: FEIE wins

A freelance designer earns $95,000 from the UAE, which has no personal income tax. She passes the Physical Presence Test with 340 days abroad and can document a real foreign tax home.

FEIE excludes the entire $95,000 — it’s under the 2026 cap. Federal income tax on that income drops to $0.

FTC wouldn’t help her: with $0 foreign tax paid, there’s nothing to credit. FEIE is the clear winner. She still owes self-employment tax on her net earnings, since FEIE doesn’t touch that (more below).

Example 2 — High-tax country: FTC wins

An employee earns $180,000 in Germany and pays roughly $65,000 in German income tax.

With FEIE alone, she could exclude $132,900 — but the remaining $47,100 would still be taxed by the US at her full-income rate (the stacking rule). And she couldn’t credit the German tax already paid on the excluded portion.

With FTC instead, her full $180,000 stays on the US return, but the $65,000 in German tax largely offsets or eliminates her US liability. Any excess credit carries forward. In a high-tax country like Germany, FTC-only frequently beats FEIE.

(Simplified for illustration. A real return would fold in brackets, deductions, and treaty provisions.)

Example 3 — Multi-country nomad: blend both

A self-employed developer splits the year across Portugal, Thailand, and Mexico — never more than a few months anywhere, spending 340 days outside the US, keeping no US lease, vehicle, or dependents. He documents client contracts and a base of operations abroad, supporting an itinerant-but-genuine foreign tax home, and passes the Physical Presence Test.

He earns $170,000 in self-employment income plus $8,000 in foreign dividends.

- FEIE excludes $132,900 of earned income.

- The remaining $37,100 in earned income plus the $8,000 in dividends stay taxable.

- Roughly $9,000 in foreign taxes withheld across his countries can be claimed as an FTC against the US tax on that remainder.

- He still owes self-employment tax on his full net earnings — and here’s the sting: of his three countries, only Portugal has a US totalization agreement. Thailand and Mexico don’t, so time worked there gives him no relief from US SE tax.

This is the realistic profile for many true nomads: FEIE handles the bulk of earned income, FTC mops up the rest.

When “combine both” is worth the complexity

Blend FEIE and FTC when your income tops the cap, you have real passive income, or your host country’s rate sits close to the US rate. If your income is comfortably under the cap and your host country has no income tax, adding FTC just adds paperwork for no benefit — stick with FEIE.

The Hidden Costs Most Guides Don’t Connect to This Decision

Self-employment tax survives FEIE

This is the single biggest misunderstanding among freelance nomads.

FEIE excludes foreign earned income from federal income tax. It does nothing to the 15.3% self-employment tax (Social Security + Medicare) on your net self-employment earnings.

Here’s the math that trips people up. SE tax applies to 92.35% of your net earnings, not the full figure.

- The 12.4% Social Security portion applies only to the first $184,500 of net earnings (2026).

- The 2.9% Medicare portion has no cap.

- High earners add a 0.9% Additional Medicare Tax above $200,000 (single) / $250,000 (MFJ).

Half of the SE tax is deductible against income — but that deduction doesn’t reduce the SE tax bill itself.

Example: A freelancer in Portugal earning $120,000 might drop federal income tax to $0 with FEIE, yet still owe roughly $17,000 in SE tax ($120,000 × 92.35% × 15.3%).

A totalization agreement between the US and your host country can sometimes exempt you from paying into both systems at once — but only if you meet that country’s residency rules under the agreement. As of 2026, the US has 30 totalization agreements in force. Many top nomad destinations — including Thailand, Mexico, the UAE, and Singapore — have none, so you keep owing US SE tax there.

You still owe estimated quarterly taxes

FEIE erasing your income tax doesn’t erase your estimated tax duty. If you’re self-employed, SE tax (and any income tax that survives FEIE/FTC) is generally due in four quarterly installments via Form 1040-ES.

The automatic June 15 extension for expats extends your filing date — not your payment date. Miss the quarterly deadlines and you can rack up underpayment penalties even while owing $0 in income tax. Budget for SE tax across the year.

The 3.8% Net Investment Income Tax (NIIT)

If you have significant passive income, watch the Net Investment Income Tax — a 3.8% surtax on investment income (dividends, interest, capital gains, rents).

- Thresholds: MAGI over $200,000 (single) / $250,000 (MFJ). These are not indexed for inflation.

- The FEIE trap: income you exclude with FEIE is added back to MAGI for the NIIT threshold. So you can owe NIIT even when your taxable income is near zero.

- The FTC trap: the Foreign Tax Credit generally cannot offset NIIT — it lives in a different part of the tax code. So foreign tax you paid on that dividend may not rescue you from this surtax.

For high-earning nomads with real portfolios, NIIT is the quiet cost that neither FEIE nor FTC fully solves.

FEIE and the Child Tax Credit trade-off

Claiming FEIE lowers your reported earned income — which can shrink or wipe out your refundable Additional Child Tax Credit (up to $1,700 per child for 2026, and only available once you show at least $2,500 in earned income).

Families with qualifying children sometimes find that FTC — which keeps earned income on the return — preserves more value overall than FEIE, even in a moderate-tax country.

FEIE and IRA / Roth IRA eligibility

IRA and Roth contributions require taxable “compensation.” If FEIE excludes all your earned income, your compensation for IRA purposes can drop to $0 — disqualifying you from contributing that year. If retirement contributions matter to you, weigh that against FEIE’s simplicity.

State tax residency — a separate battle

Your federal FEIE or FTC choice has zero effect on whether your home state still calls you a resident.

States vary widely. Some use bright-line day counts; others weigh domicile and intent. A handful of “sticky” states — California, New York, New Mexico, Virginia, and South Carolina — are known for pursuing residency based on retained property, bank accounts, or ongoing ties. Clean-exit domicile states like Florida, Texas, Washington, Nevada, and South Dakota have no state income tax at all.

Severing state ties (driver’s license, voter registration, banking, mailing address) is a separate project from your federal filing — and getting it wrong can cost more than an imperfect FEIE/FTC call.

What Changed for 2026 (and Why It Affects Your Decision)

The One Big Beautiful Bill Act (OBBBA), signed July 4, 2025, made the 2017 tax cuts permanent — including the top 37% rate and higher standard deductions.

For 2026, the standard deduction is $16,100 (single), $32,200 (married filing jointly), and $24,150 (head of household). Pair that with the rising FEIE cap ($132,900), and many single filers earning moderate six figures in a low-tax country land at or near $0 federal income tax.

The remittance tax — mostly overstated for nomads

You may have seen headlines about a 1% federal excise tax on outbound remittance transfers under IRC Section 4475, effective for transfers made after December 31, 2025. Be precise about what it covers, because it’s constantly exaggerated.

- It applies only to transfers funded by physical cash, money orders, or cashier’s checks sent from the US.

- Transfers funded by a bank withdrawal or a debit/credit card are exempt. Under proposed regulations issued in April 2026, that card exemption was clarified to cover any debit or credit card, regardless of where it was issued (traveler’s checks were added to the taxable list).

For the vast majority of digital nomads — who move money by bank transfer, fintech app, or card — this tax simply doesn’t apply to how they actually move money. It matters far more for cash-based remittance senders than for nomads managing income digitally.

Can You Switch Between FEIE and FTC Later?

The 5-year revocation lockout

Once you elect FEIE, you can’t casually flip back and forth. If you revoke it, you generally can’t re-elect FEIE for five years without IRS approval. That makes FEIE a longer-term commitment, not a year-to-year toggle.

When switching makes sense

If your situation genuinely changes — you move from a low-tax country to a high-tax one, or your income rockets past the cap — the math can shift enough that giving up FEIE for FTC becomes worth it, lockout and all. Model it carefully before committing, because reversing it is neither quick nor guaranteed.

How to model the switch first

Run both scenarios side by side with your real numbers: current income, host-country rate, income trajectory, and family situation. If FTC saves you meaningfully more over several years — not just this one — it may be worth the lockout. If it’s a close call, staying put usually beats triggering a five-year restriction for a marginal gain.

Behind on Filing? How to Catch Up Without Penalties

Plenty of nomads discover their filing duties years after going location-independent. The IRS’s Streamlined Filing Compliance Procedures exist for exactly this.

Who qualifies

You generally qualify for the foreign version (Streamlined Foreign Offshore Procedures) if:

- You didn’t have a US abode, and

- You were physically outside the US for at least 330 full days in one or more of the most recent tax years for which the return due date has passed, and

- Your failure to file was non-willful — a genuine misunderstanding, not intentional avoidance.

What “non-willful” means, and Form 14653

You certify non-willfulness on Form 14653, explaining the facts behind your failure to file. This isn’t a formality. The IRS reviews these certifications, and a weak or inconsistent story can sink the whole submission.

The catch-up process, step by step

- Confirm you meet the non-residency and non-willfulness tests — and that you’re not already under IRS audit or criminal investigation for those years.

- File the last 3 years of delinquent or amended US returns, claiming FEIE, FTC, or other benefits you’re owed.

- File the last 6 years of delinquent FBARs electronically through the FinCEN BSA e-filing system, if you had foreign accounts over the threshold.

- Submit Form 14653 with your non-willful certification.

- Mark submissions correctly per IRS instructions, so they’re processed under the streamlined program — not as ordinary late filings.

Why acting before contact matters

The program is voluntary, and that’s the whole basis for its leniency. Once the IRS reaches out to you about missing returns, the streamlined option is generally gone. If you’re behind, the cost of waiting only grows.

Your Digital Nomad Tax Filing Checklist

Core forms

| Form | Purpose |

|---|---|

| Form 1040 | Your main US individual income tax return |

| Schedule C | Reports self-employment business income and expenses |

| Schedule SE | Calculates self-employment tax |

| Form 2555 | Claims FEIE and the foreign housing exclusion/deduction |

| Form 1116 | Claims the Foreign Tax Credit |

| Form 1040-ES | Pays estimated quarterly taxes (SE tax + surviving income tax) |

| Form 8960 | Calculates the Net Investment Income Tax, if it applies |

Information returns (no tax owed — but real penalties for skipping them)

- FBAR (FinCEN Form 114) — required if your combined foreign account balances topped $10,000 at any point in the year.

- Form 8938 (FATCA) — required if your foreign financial assets exceed certain thresholds, which vary by filing status and residency.

Key deadlines

- April 15 — standard filing deadline; any tax owed is due now, even with an extension.

- June 15 — automatic 2-month extension for citizens/residents abroad, granted without a request (filing only, not payment).

- October 15 — further extension by filing Form 4868 before the June deadline.

- FBAR — due April 15, with an automatic extension to October 15.

- Quarterly (roughly April 15, June 15, Sept 15, Jan 15) — estimated tax installments via Form 1040-ES.

A Note on This Guide

This article explains how FEIE and FTC generally work, for general educational purposes. It is not personalized tax advice.

Tax outcomes depend on your specific facts — income type, country of residence, family situation, and long-term plans. Getting the tax-home and abode analysis wrong can be expensive to unwind. For anything beyond the simplest case (one country, income under the cap, no dependents), model both scenarios with a qualified tax professional. It’s worth the cost.

FAQs

Can I use FEIE and FTC in the same year?

Yes, but never on the same dollar of income. Exclude earned income with FEIE, then claim FTC on income above the cap or on passive income.

Does FEIE reduce self-employment tax?

No. FEIE only reduces federal income tax on excluded earnings. Self-employment tax (about 15.3%) still applies to your net self-employment income, regardless of FEIE.

Do I have to file if I earn under the FEIE limit?

Yes — if your worldwide gross income meets the filing threshold for your status, which is far lower than the FEIE cap. Filing is what lets you claim the exclusion in the first place.

What counts as a “tax home” for a digital nomad?

It’s the general area of your main place of business abroad — not where you sleep. You also need your abode (your strongest personal, family, and economic ties) to be outside the US. Move constantly with no base, and the IRS may treat you as an “itinerant,” which raises the documentation bar.

Does a US employer disqualify me from FEIE?

No. What matters is where the work is performed and where your abode sits — not whose payroll you’re on. A US employee working full-time and indefinitely from abroad can still qualify.

What if I don’t have a fixed home base — can I still qualify?

Often yes, using the Physical Presence Test rather than the Bona Fide Residence Test. But you’ll need solid documentation to support your tax home and abode, since “itinerant” filers face more scrutiny.

How many days can I spend in the US and still use FEIE?

On the Physical Presence Test, you need 330 full days in foreign countries within a 12-month window — so US days directly eat into your count. Roughly 35 US days is the ceiling before you fail the test.

Is FEIE or FTC better if I have kids?

FTC is often better for families. FEIE can reduce or eliminate the refundable Additional Child Tax Credit (up to $1,700 per child in 2026) by lowering your reported earned income.

Do digital nomads pay US state taxes?

Maybe. Your federal FEIE/FTC choice doesn’t settle state residency. “Sticky” states like California and New York may still tax you until you properly cut ties. No-income-tax domicile states like Florida and Texas avoid the issue entirely.

Conclusion

For digital nomads, FEIE vs FTC isn’t really the first question. It’s the second.

The first is whether you can establish a foreign tax home at all — given how often nomads move. Once that’s settled, the choice between excluding income (FEIE) and crediting foreign tax (FTC) usually comes down to your host country’s rate, your income level, and whether you have passive income or dependents in the mix. Many nomads end up using both.

Whatever you choose, the self-employment tax, the NIIT, and your state residency don’t vanish just because your federal income tax does. Plan for those separately — and don’t treat this year’s election as something you can casually reverse next year.

Sources & References

- IRS – Foreign Earned Income Exclusion

- IRS – Figuring the Foreign Earned Income Exclusion

- IRS Publication 54 – Tax Guide for U.S. Citizens and Resident Aliens Abroad

- IRS – U.S. Citizens and Resident Aliens Abroad

- IRS – U.S. Citizens and Residents Abroad Filing Requirements

- IRS Instructions for Form 1116 (Foreign Tax Credit)

- IRS Instructions for Form 2555 (Foreign Earned Income Exclusion)

- IRS – Net Investment Income Tax (Q&A)

- IRS – Estimated Taxes

- IRS – Streamlined Filing Compliance Procedures

- IRS – Streamlined Foreign Offshore Procedures

- IRS Notice 2025-55 (Remittance Transfer Excise Tax Penalty Relief)

- Federal Register – Excise Tax on Remittance Transfers (Proposed Rule)

- Social Security Administration – Totalization Agreements Overview

- Becker Professional Education – Remote Work Tax Guide

- Fox Rothschild – Tax Court Broadens Foreign Earned Income Exclusion

This article is for general informational purposes only and is not immigration or tax advice. Rules and figures are current as of July 2026 and change often. Consult a licensed immigration lawyer and a qualified tax professional for guidance on your specific situation.

Anjali Kaur is a finance writer specializing in personal finance, international tax, and financial planning for digital nomads, expats, and remote workers. She breaks down dense, high-stakes topics — the Foreign Earned Income Exclusion, totalization agreements, tax residency, and visa-linked tax breaks — into plain-language guides that help readers make confident decisions. Her approach is research-led and source-driven: every figure is dated, and she flags where rules vary or have recently changed. Anjali fact-checks her finance and tax coverage against primary sources such as the IRS, the SSA, and official government tax authorities. Connect with her on Facebook or read more of her work in the Finance section.